In government contracting, “compliant” is often treated as synonymous with “safe.”

If the Basis of Estimate (BOE) follows the required format, includes labor categories, hours, rates, and summary calculations, many teams assume the risk is low. The boxes are checked. The math ties. The sections are filled in.

And yet, audits still fail.

Not because the estimate was fraudulent.

Not because the numbers were wildly unrealistic.

But because compliance alone is not credibility.

There is a difference.

The Illusion of Compliance

A BOE can be technically compliant and still collapse under scrutiny.

Why?

Because compliance focuses on structure.

Audits focus on reasoning.

A compliant BOE might include:

- Labor categories and hours

- Historical references

- Escalation assumptions

- Indirect rates

- Narrative explanations

But auditors are not testing whether the sections exist. They are testing whether the logic holds together.

That’s where most BOEs fail.

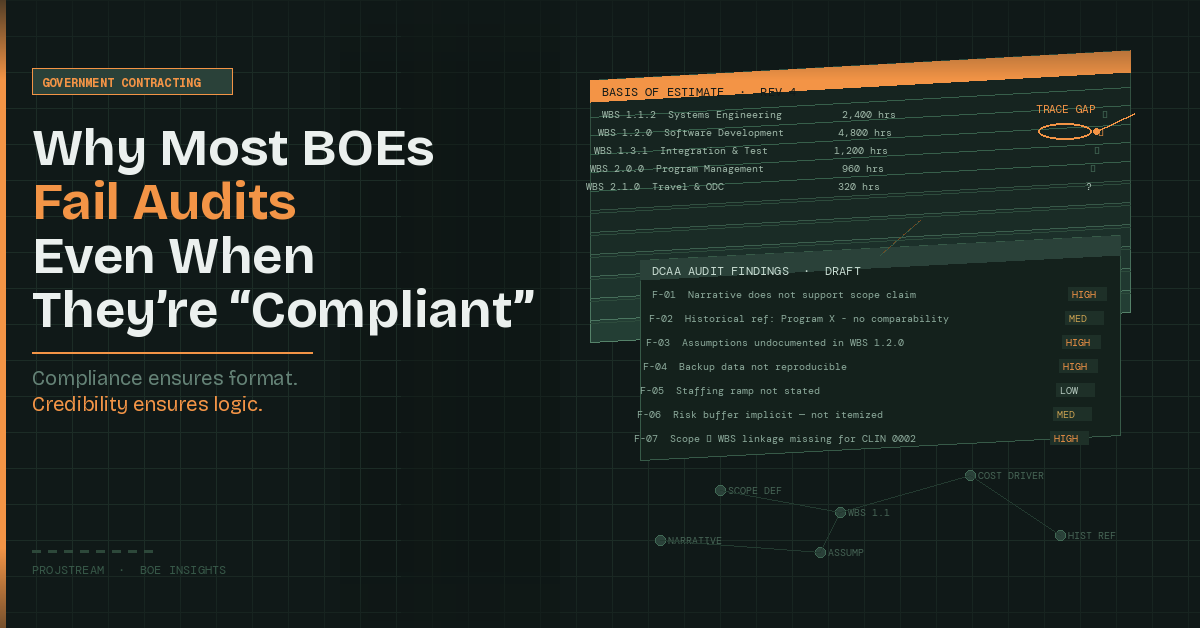

Where “Compliant” BOEs Break Down

Narrative Gaps

One of the most common failure points is the gap between numbers and explanation.

A BOE might state:

2,400 engineering hours based on historical program X.

But the auditor’s next questions are immediate:

- What was the scope on Program X?

- How is it comparable to this effort?

- What adjustments were made?

- Why are those adjustments reasonable?

If the narrative does not explicitly connect the historical reference to the current scope, the estimate looks recycled rather than reasoned.

Compliance requires a narrative.

Audit defensibility requires a coherent story.

Those are not the same thing.

Assumptions That Aren’t Explicit

Every estimate is built on assumptions. The problem is that many BOEs treat them as background context rather than structural elements.

Common issues include:

- Implicit scope exclusions

- Undefined productivity factors

- Unstated staffing ramps

- Hidden risk buffers

During an audit, assumptions that are not clearly documented become vulnerabilities. Auditors will ask:

- Where is that assumption documented?

- Who approved it?

- What data supports it?

- Is it consistent across the estimate?

If assumptions are scattered across spreadsheets, emails, and institutional memory, the BOE may be compliant in format but fragile in substance.

Traceability Breaks

This is the failure mode that surprises most teams.

The hours tie to the summary.

The rates tie to the forward pricing rate agreement.

The totals reconcile.

And still, the BOE fails.

Why?

Because traceability is incomplete.

Auditors test whether they can move cleanly through the estimate chain:

Scope → WBS → Estimate → Narrative → Backup Data

If any link is weak, the entire structure becomes questionable.

For example:

- The narrative describes one scope interpretation, but the WBS reflects another.

- The estimate references historical data, but the backup cannot be reproduced.

- The hours are allocated at the work package level, but the justification is written at a higher level of abstraction.

These aren’t compliance violations. They are structural inconsistencies.

And auditors notice.

The Auditor’s Perspective

It helps to understand what an audit is actually testing.

Auditors are not trying to “catch” estimators. They are trying to answer a simple question:

Can this estimate be understood, reproduced, and defended by someone other than the original author?

That means they evaluate:

- Logical consistency

- Evidence alignment

- Internal traceability

- Clear attribution of data sources

- Explicit reasoning behind adjustments

If the BOE depends on informal knowledge, undocumented judgment calls, or manually reconciled spreadsheets, it becomes difficult to defend—even if the math is correct.

Why This Problem Persists

Estimating Is Often Spreadsheet-First

Many organizations build the numbers first and write the narrative later. The narrative becomes an explanation of outputs rather than a structured reflection of inputs.

That inversion creates gaps.

When cost reasoning is not captured during estimating, it must be reconstructed afterward. Reconstruction is rarely as precise as original intent.

Data Is Scattered

Historical references may exist in:

- Prior proposals

- Contract performance reports

- Independent spreadsheets

- Individual estimator files

If the linkage between source data and estimate logic is not preserved, audit defense becomes manual and time-consuming.

In high-pressure proposal environments, that’s where inconsistencies creep in.

Traceability Is Treated as Administrative

Many teams view traceability as a documentation requirement rather than a structural design principle.

But traceability is not paperwork. It is architecture.

When estimates are built without persistent links between:

- Scope definitions

- WBS elements

- Cost drivers

- Historical references

- Assumptions

The BOE becomes a collection of artifacts rather than an integrated system.

Compliance checks artifacts.

Audits test systems.

What Audit-Resilient BOEs Actually Look Like

Assumptions Are Structured, Not Implied

Assumptions are captured as discrete elements tied to scope and cost drivers, not buried in narrative paragraphs.

Historical References Are Comparable and Adjusted

The BOE clearly explains:

- Why the historical effort is relevant

- What changed

- How adjustments were calculated

Scope Mapping Is Explicit

Requirements or scope elements map cleanly to WBS elements and work packages. The estimate reflects that structure.

The Narrative Mirrors the Estimate Structure

The story follows the same hierarchy as the cost build-up. Reviewers don’t have to translate between formats.

Backup Is Reproducible

An independent reviewer can follow the logic without relying on institutional memory.

When those conditions exist, audits become confirmations rather than interrogations.

The Strategic Impact of Audit Failure

Audit failure is not just a compliance inconvenience. It has broader consequences:

- Increased review cycles

- Delayed negotiations

- Reduced evaluator confidence

- Elevated risk perceptions

- Margin pressure

In competitive environments, credibility compounds. Teams that consistently submit audit-resilient BOEs build reputational capital with contracting officers and auditors.

Teams that repeatedly require clarification or rework build the opposite.

Moving Beyond “Compliant” to Defensible

The solution is not more documentation. It is better structure.

That means:

- Capturing assumptions during estimating, not after

- Linking historical data directly to cost elements

- Preserving requirement-to-cost lineage

- Designing BOEs around traceability from the start

- Treating the narrative as part of the estimate, not a summary of it

When estimating is structured around traceability, compliance becomes a natural byproduct rather than the objective.

When BOEs, assumptions, and historical references are captured in a structured, connected environment—rather than scattered across files—the audit story is already embedded in the estimate itself.

Instead of reconstructing reasoning during review, teams can demonstrate it.

Closing Thought

Most BOEs don’t fail audits because they are wrong.

They fail because they are disconnected.

Disconnected from scope.

Disconnected from historical context.

Disconnected from their own assumptions.

Compliance ensures the format is acceptable.

Credibility ensures the logic is defensible.

And in government contracting, credibility is what survives an audit.

{kind=link}

{kind=link}